@resreassure

25Robert is part-Canadian, part-British, somewhat autistic and lives in Geneva. He is going to link the crypto system to the real economy.

steemit.com/@resreassureVOTING POWER100.00%

DOWNVOTE POWER100.00%

RESOURCE CREDITS100.00%

REPUTATION PROGRESS0.00%

Net Worth

0.000USD

STEEM

0.000STEEM

SBD

0.000SBD

Effective Power

1.201SP

├── Own SP

0.000SP

└── Incoming DelegationsDeleg

+1.201SP

Detailed Balance

| STEEM | ||

| balance | 0.000STEEM | STEEM |

| market_balance | 0.000STEEM | STEEM |

| savings_balance | 0.000STEEM | STEEM |

| reward_steem_balance | 0.000STEEM | STEEM |

| STEEM POWER | ||

| Own SP | 0.000SP | SP |

| Delegated Out | 0.000SP | SP |

| Delegation In | 1.201SP | SP |

| Effective Power | 1.201SP | SP |

| Reward SP (pending) | 0.000SP | SP |

| SBD | ||

| sbd_balance | 0.000SBD | SBD |

| sbd_conversions | 0.000SBD | SBD |

| sbd_market_balance | 0.000SBD | SBD |

| savings_sbd_balance | 0.000SBD | SBD |

| reward_sbd_balance | 0.000SBD | SBD |

{

"balance": "0.000 STEEM",

"savings_balance": "0.000 STEEM",

"reward_steem_balance": "0.000 STEEM",

"vesting_shares": "0.000000 VESTS",

"delegated_vesting_shares": "0.000000 VESTS",

"received_vesting_shares": "1953.311140 VESTS",

"sbd_balance": "0.000 SBD",

"savings_sbd_balance": "0.000 SBD",

"reward_sbd_balance": "0.000 SBD",

"conversions": []

}Account Info

| name | resreassure |

| id | 1186811 |

| rank | 1,587,034 |

| reputation | 58365719 |

| created | 2019-01-05T13:59:39 |

| recovery_account | steem |

| proxy | None |

| post_count | 6 |

| comment_count | 0 |

| lifetime_vote_count | 0 |

| witnesses_voted_for | 0 |

| last_post | 2019-01-09T18:10:09 |

| last_root_post | 2019-01-09T18:10:09 |

| last_vote_time | 1970-01-01T00:00:00 |

| proxied_vsf_votes | 0, 0, 0, 0 |

| can_vote | 1 |

| voting_power | 0 |

| delayed_votes | 0 |

| balance | 0.000 STEEM |

| savings_balance | 0.000 STEEM |

| sbd_balance | 0.000 SBD |

| savings_sbd_balance | 0.000 SBD |

| vesting_shares | 0.000000 VESTS |

| delegated_vesting_shares | 0.000000 VESTS |

| received_vesting_shares | 1953.311140 VESTS |

| reward_vesting_balance | 0.000000 VESTS |

| vesting_balance | 0.000 STEEM |

| vesting_withdraw_rate | 0.000000 VESTS |

| next_vesting_withdrawal | 1969-12-31T23:59:59 |

| withdrawn | 0 |

| to_withdraw | 0 |

| withdraw_routes | 0 |

| savings_withdraw_requests | 0 |

| last_account_recovery | 1970-01-01T00:00:00 |

| reset_account | null |

| last_owner_update | 1970-01-01T00:00:00 |

| last_account_update | 2019-01-05T14:04:06 |

| mined | No |

| sbd_seconds | 0 |

| sbd_last_interest_payment | 1970-01-01T00:00:00 |

| savings_sbd_last_interest_payment | 1970-01-01T00:00:00 |

{

"id": 1186811,

"name": "resreassure",

"owner": {

"weight_threshold": 1,

"account_auths": [],

"key_auths": [

[

"STM56uFJnyi1X7s9eCnGNZ8TvM4BSDsZb8tK5FfXHhy6YfLEfgqSX",

1

]

]

},

"active": {

"weight_threshold": 1,

"account_auths": [],

"key_auths": [

[

"STM7caCVFiLHKKnNbgkxHQsEmCnc7U6oLohsRm2xaDq1xqGtneUbp",

1

]

]

},

"posting": {

"weight_threshold": 1,

"account_auths": [],

"key_auths": [

[

"STM6QDSMt7p8ky7caJTFAK1nW5y7dttxo9gHwFqdBFxWtmXDVRPYw",

1

]

]

},

"memo_key": "STM7bEsEXEdHkkfxL8iCt67xmcLMLH5pk31FitDPkTgJndLnVFGq6",

"json_metadata": "{\"profile\":{\"profile_image\":\"https://cdn.steemitimages.com/DQmeimm3NbyND9fdLwR4kRb4CCCPeayBrGj9dnoQz12RjpR/RES%20photo.png\",\"name\":\"Robert Sharratt\",\"about\":\"Robert is part-Canadian, part-British, somewhat autistic and lives in Geneva. He is going to link the crypto system to the real economy.\",\"location\":\"Geneva, Switzerland\",\"website\":\"https://reassurefinancial.com\"}}",

"posting_json_metadata": "{\"profile\":{\"profile_image\":\"https://cdn.steemitimages.com/DQmeimm3NbyND9fdLwR4kRb4CCCPeayBrGj9dnoQz12RjpR/RES%20photo.png\",\"name\":\"Robert Sharratt\",\"about\":\"Robert is part-Canadian, part-British, somewhat autistic and lives in Geneva. He is going to link the crypto system to the real economy.\",\"location\":\"Geneva, Switzerland\",\"website\":\"https://reassurefinancial.com\"}}",

"proxy": "",

"last_owner_update": "1970-01-01T00:00:00",

"last_account_update": "2019-01-05T14:04:06",

"created": "2019-01-05T13:59:39",

"mined": false,

"recovery_account": "steem",

"last_account_recovery": "1970-01-01T00:00:00",

"reset_account": "null",

"comment_count": 0,

"lifetime_vote_count": 0,

"post_count": 6,

"can_vote": true,

"voting_manabar": {

"current_mana": 1953311140,

"last_update_time": 1588949421

},

"downvote_manabar": {

"current_mana": 488327785,

"last_update_time": 1588949421

},

"voting_power": 0,

"balance": "0.000 STEEM",

"savings_balance": "0.000 STEEM",

"sbd_balance": "0.000 SBD",

"sbd_seconds": "0",

"sbd_seconds_last_update": "1970-01-01T00:00:00",

"sbd_last_interest_payment": "1970-01-01T00:00:00",

"savings_sbd_balance": "0.000 SBD",

"savings_sbd_seconds": "0",

"savings_sbd_seconds_last_update": "1970-01-01T00:00:00",

"savings_sbd_last_interest_payment": "1970-01-01T00:00:00",

"savings_withdraw_requests": 0,

"reward_sbd_balance": "0.000 SBD",

"reward_steem_balance": "0.000 STEEM",

"reward_vesting_balance": "0.000000 VESTS",

"reward_vesting_steem": "0.000 STEEM",

"vesting_shares": "0.000000 VESTS",

"delegated_vesting_shares": "0.000000 VESTS",

"received_vesting_shares": "1953.311140 VESTS",

"vesting_withdraw_rate": "0.000000 VESTS",

"next_vesting_withdrawal": "1969-12-31T23:59:59",

"withdrawn": 0,

"to_withdraw": 0,

"withdraw_routes": 0,

"curation_rewards": 0,

"posting_rewards": 0,

"proxied_vsf_votes": [

0,

0,

0,

0

],

"witnesses_voted_for": 0,

"last_post": "2019-01-09T18:10:09",

"last_root_post": "2019-01-09T18:10:09",

"last_vote_time": "1970-01-01T00:00:00",

"post_bandwidth": 0,

"pending_claimed_accounts": 0,

"vesting_balance": "0.000 STEEM",

"reputation": 58365719,

"transfer_history": [],

"market_history": [],

"post_history": [],

"vote_history": [],

"other_history": [],

"witness_votes": [],

"tags_usage": [],

"guest_bloggers": [],

"rank": 1587034

}Withdraw Routes

| Incoming | Outgoing |

|---|---|

Empty | Empty |

{

"incoming": [],

"outgoing": []

}From Date

To Date

steemdelegated 1.201 SP to @resreassure2020/05/08 14:50:21

steemdelegated 1.201 SP to @resreassure

2020/05/08 14:50:21

| delegator | steem |

| delegatee | resreassure |

| vesting shares | 1953.311140 VESTS |

| Transaction Info | Block #43199577/Trx ae206ab8355fa52471266d5f1c7731f909c7b3c5 |

View Raw JSON Data

{

"trx_id": "ae206ab8355fa52471266d5f1c7731f909c7b3c5",

"block": 43199577,

"trx_in_block": 23,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2020-05-08T14:50:21",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "resreassure",

"vesting_shares": "1953.311140 VESTS"

}

]

}steemdelegated 6.023 SP to @resreassure2020/03/10 01:30:15

steemdelegated 6.023 SP to @resreassure

2020/03/10 01:30:15

| delegator | steem |

| delegatee | resreassure |

| vesting shares | 9797.170121 VESTS |

| Transaction Info | Block #41516275/Trx 1931795b81adc829c92c0574d6d48132efd22d74 |

View Raw JSON Data

{

"trx_id": "1931795b81adc829c92c0574d6d48132efd22d74",

"block": 41516275,

"trx_in_block": 11,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2020-03-10T01:30:15",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "resreassure",

"vesting_shares": "9797.170121 VESTS"

}

]

}2020/01/05 14:42:09

2020/01/05 14:42:09

| parent author | resreassure |

| parent permlink | why-do-people-buy-bitcoin |

| author | steemitboard |

| permlink | steemitboard-notify-resreassure-20200105t144208000z |

| title | |

| body | Congratulations @resreassure! You received a personal award! <table><tr><td>https://steemitimages.com/70x70/http://steemitboard.com/@resreassure/birthday1.png</td><td>Happy Birthday! - You are on the Steem blockchain for 1 year!</td></tr></table> <sub>_You can view [your badges on your Steem Board](https://steemitboard.com/@resreassure) and compare to others on the [Steem Ranking](https://steemitboard.com/ranking/index.php?name=resreassure)_</sub> ###### [Vote for @Steemitboard as a witness](https://v2.steemconnect.com/sign/account-witness-vote?witness=steemitboard&approve=1) to get one more award and increased upvotes! |

| json metadata | {"image":["https://steemitboard.com/img/notify.png"]} |

| Transaction Info | Block #39664940/Trx 1325e585562d8cda14413a81dd1987e56621fc7a |

View Raw JSON Data

{

"trx_id": "1325e585562d8cda14413a81dd1987e56621fc7a",

"block": 39664940,

"trx_in_block": 8,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2020-01-05T14:42:09",

"op": [

"comment",

{

"parent_author": "resreassure",

"parent_permlink": "why-do-people-buy-bitcoin",

"author": "steemitboard",

"permlink": "steemitboard-notify-resreassure-20200105t144208000z",

"title": "",

"body": "Congratulations @resreassure! You received a personal award!\n\n<table><tr><td>https://steemitimages.com/70x70/http://steemitboard.com/@resreassure/birthday1.png</td><td>Happy Birthday! - You are on the Steem blockchain for 1 year!</td></tr></table>\n\n<sub>_You can view [your badges on your Steem Board](https://steemitboard.com/@resreassure) and compare to others on the [Steem Ranking](https://steemitboard.com/ranking/index.php?name=resreassure)_</sub>\n\n\n###### [Vote for @Steemitboard as a witness](https://v2.steemconnect.com/sign/account-witness-vote?witness=steemitboard&approve=1) to get one more award and increased upvotes!",

"json_metadata": "{\"image\":[\"https://steemitboard.com/img/notify.png\"]}"

}

]

}steemdelegated 6.144 SP to @resreassure2019/04/10 18:46:45

steemdelegated 6.144 SP to @resreassure

2019/04/10 18:46:45

| delegator | steem |

| delegatee | resreassure |

| vesting shares | 9993.157563 VESTS |

| Transaction Info | Block #31930263/Trx 311a2111cadd21da1e13327d467e8611d90217d0 |

View Raw JSON Data

{

"trx_id": "311a2111cadd21da1e13327d467e8611d90217d0",

"block": 31930263,

"trx_in_block": 7,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-04-10T18:46:45",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "resreassure",

"vesting_shares": "9993.157563 VESTS"

}

]

}2019/02/26 02:43:06

2019/02/26 02:43:06

| parent author | resreassure |

| parent permlink | why-do-people-buy-bitcoin |

| author | partiko |

| permlink | partiko-re-resreassure-why-do-people-buy-bitcoin-20190226t024306061z |

| title | |

| body | Hello @resreassure! This is a friendly reminder that you have 3000 Partiko Points unclaimed in your Partiko account! Partiko is a fast and beautiful mobile app for Steem, and it’s the most popular Steem mobile app out there! Download Partiko using the link below and login using SteemConnect to claim your 3000 Partiko points! You can easily convert them into Steem token! https://partiko.app/referral/partiko  |

| json metadata | {"app":"partiko"} |

| Transaction Info | Block #30673784/Trx b0120af68e1f5eaf49ea67c23b9f94a76e294a00 |

View Raw JSON Data

{

"trx_id": "b0120af68e1f5eaf49ea67c23b9f94a76e294a00",

"block": 30673784,

"trx_in_block": 21,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-02-26T02:43:06",

"op": [

"comment",

{

"parent_author": "resreassure",

"parent_permlink": "why-do-people-buy-bitcoin",

"author": "partiko",

"permlink": "partiko-re-resreassure-why-do-people-buy-bitcoin-20190226t024306061z",

"title": "",

"body": "Hello @resreassure! This is a friendly reminder that you have 3000 Partiko Points unclaimed in your Partiko account!\n\nPartiko is a fast and beautiful mobile app for Steem, and it’s the most popular Steem mobile app out there! Download Partiko using the link below and login using SteemConnect to claim your 3000 Partiko points! You can easily convert them into Steem token!\n\nhttps://partiko.app/referral/partiko\n\n",

"json_metadata": "{\"app\":\"partiko\"}"

}

]

}steemdelegated 18.504 SP to @resreassure2019/01/31 20:02:12

steemdelegated 18.504 SP to @resreassure

2019/01/31 20:02:12

| delegator | steem |

| delegatee | resreassure |

| vesting shares | 30098.578710 VESTS |

| Transaction Info | Block #29946360/Trx ea3ddb431e67413c9ab14c7f0bc1b497b4e31dbb |

View Raw JSON Data

{

"trx_id": "ea3ddb431e67413c9ab14c7f0bc1b497b4e31dbb",

"block": 29946360,

"trx_in_block": 31,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-31T20:02:12",

"op": [

"delegate_vesting_shares",

{

"delegator": "steem",

"delegatee": "resreassure",

"vesting_shares": "30098.578710 VESTS"

}

]

}2019/01/11 12:18:27

2019/01/11 12:18:27

| parent author | resreassure |

| parent permlink | crypto-and-sex |

| author | steemcleaners |

| permlink | re-resreassure-crypto-and-sex-20190111t121825278z |

| title | |

| body | [Source](https://medium.com/@res_reassure/omgno-crypto-and-womens-sexual-pleasure-74dd99db6bbe) [Plagiarism](http://www.plagiarism.org/plagiarism-101/what-is-plagiarism/) is the copying & pasting of others work without giving credit to the original author or artist. Plagiarized posts are considered spam. Spam is discouraged by the community, and may result in action from the [cheetah bot](https://steemit.com/faq.html#What_is__cheetah). [More information and tips on sharing content.](https://steemcleaners.org/copy-paste-plagiarism/) If you believe this comment is in error, please contact us in [#disputes on Discord](https://discord.gg/YR2Wy5A) |

| json metadata | {"app":"steemcleaners/0.3","format":"markdown+html","community":"steemcleaners"} |

| Transaction Info | Block #29361662/Trx 8a9ba7844034df874246d9930f0c04e43e401639 |

View Raw JSON Data

{

"trx_id": "8a9ba7844034df874246d9930f0c04e43e401639",

"block": 29361662,

"trx_in_block": 3,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-11T12:18:27",

"op": [

"comment",

{

"parent_author": "resreassure",

"parent_permlink": "crypto-and-sex",

"author": "steemcleaners",

"permlink": "re-resreassure-crypto-and-sex-20190111t121825278z",

"title": "",

"body": "[Source](https://medium.com/@res_reassure/omgno-crypto-and-womens-sexual-pleasure-74dd99db6bbe)\n[Plagiarism](http://www.plagiarism.org/plagiarism-101/what-is-plagiarism/) is the copying & pasting of others work without giving credit to the original author or artist. Plagiarized posts are considered spam. \r\n\r\nSpam is discouraged by the community, and may result in action from the [cheetah bot](https://steemit.com/faq.html#What_is__cheetah).\r\n\r\n[More information and tips on sharing content.](https://steemcleaners.org/copy-paste-plagiarism/)\r\n\r\nIf you believe this comment is in error, please contact us in [#disputes on Discord](https://discord.gg/YR2Wy5A)",

"json_metadata": "{\"app\":\"steemcleaners/0.3\",\"format\":\"markdown+html\",\"community\":\"steemcleaners\"}"

}

]

}mikitsupvoted (100.00%) @resreassure / why-do-people-buy-bitcoin2019/01/09 18:40:30

mikitsupvoted (100.00%) @resreassure / why-do-people-buy-bitcoin

2019/01/09 18:40:30

| voter | mikits |

| author | resreassure |

| permlink | why-do-people-buy-bitcoin |

| weight | 10000 (100.00%) |

| Transaction Info | Block #29311725/Trx 9d8a20bc4bc81849b9b797a8e923f527b9a3e878 |

View Raw JSON Data

{

"trx_id": "9d8a20bc4bc81849b9b797a8e923f527b9a3e878",

"block": 29311725,

"trx_in_block": 9,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-09T18:40:30",

"op": [

"vote",

{

"voter": "mikits",

"author": "resreassure",

"permlink": "why-do-people-buy-bitcoin",

"weight": 10000

}

]

}muhammad69upvoted (100.00%) @resreassure / why-do-people-buy-bitcoin2019/01/09 18:12:51

muhammad69upvoted (100.00%) @resreassure / why-do-people-buy-bitcoin

2019/01/09 18:12:51

| voter | muhammad69 |

| author | resreassure |

| permlink | why-do-people-buy-bitcoin |

| weight | 10000 (100.00%) |

| Transaction Info | Block #29311172/Trx 3b49bc0cbb3a423787ff3243fc8ca30a96839447 |

View Raw JSON Data

{

"trx_id": "3b49bc0cbb3a423787ff3243fc8ca30a96839447",

"block": 29311172,

"trx_in_block": 18,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-09T18:12:51",

"op": [

"vote",

{

"voter": "muhammad69",

"author": "resreassure",

"permlink": "why-do-people-buy-bitcoin",

"weight": 10000

}

]

}resreassureupdated options for why-do-people-buy-bitcoin2019/01/09 18:10:09

resreassureupdated options for why-do-people-buy-bitcoin

2019/01/09 18:10:09

| author | resreassure |

| permlink | why-do-people-buy-bitcoin |

| max accepted payout | 0.000 SBD |

| percent steem dollars | 10000 |

| allow votes | true |

| allow curation rewards | true |

| extensions | [] |

| Transaction Info | Block #29311118/Trx fca004665a9758bdb3eeda921ee9e8db87b8f8ae |

View Raw JSON Data

{

"trx_id": "fca004665a9758bdb3eeda921ee9e8db87b8f8ae",

"block": 29311118,

"trx_in_block": 28,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-09T18:10:09",

"op": [

"comment_options",

{

"author": "resreassure",

"permlink": "why-do-people-buy-bitcoin",

"max_accepted_payout": "0.000 SBD",

"percent_steem_dollars": 10000,

"allow_votes": true,

"allow_curation_rewards": true,

"extensions": []

}

]

}resreassurepublished a new post: why-do-people-buy-bitcoin2019/01/09 18:10:09

resreassurepublished a new post: why-do-people-buy-bitcoin

2019/01/09 18:10:09

| parent author | |

| parent permlink | bitcoin |

| author | resreassure |

| permlink | why-do-people-buy-bitcoin |

| title | Why do people buy bitcoin? |

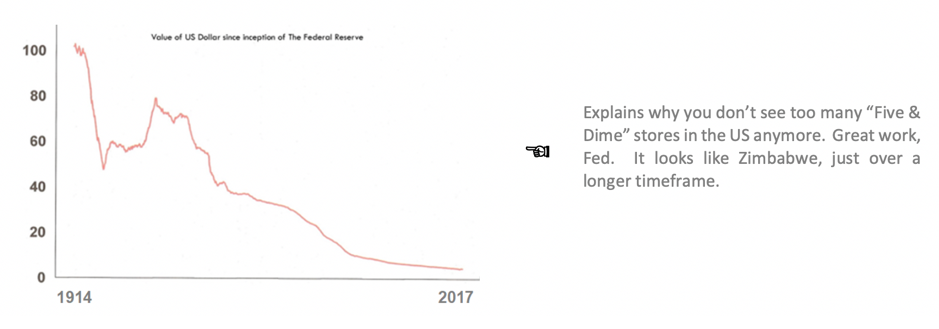

| body | Why bitcoin? People buy bitcoin because of value and values. People buy bitcoin because it is a system of money that corresponds to how humanity has exchanged value for most of our history. Technologically, this system is based on mathematical formulae and a straight-forward verification and record system. The implications are spectacular: you can now trust exchanging value with another person or institution directly, even if you don’t know them. In terms of values, the crypto system is profoundly natural, a very human invention, based on the concepts of freedom and fairness. It is the most authentic form of money humanity has had since value was based on memory. It is characterised as set out below. Based only on PV money (i.e. value that exists today, not tied to any required future value creation). Allows value to be exchanged directly between two parties without any bank middlemen, almost instantaneously and at extremely low cost. A better description than the term crypto currencies is honest money. This money system is about more than just exchanging value; it is also about our values. The crypto system is digital technology to banking and paper money’s analogue technology. The potential, the combination of value and values, that this new (old really) system unlocks for humanity is hard to overstate. The fractional reserve banking system is intrinsically dishonest: bankers will tell you that your money is both safely in the bank and, at the same time, they are lending it out to others. They will tell you that it is your money while, legally, it belongs to the bank and they can do what they want with it.  Why is bitcoin superior to other currencies? Bitcoin is a superior product to nation state currency and the fractional reserve banking system, for these reasons: 1. lower cost (transaction costs much lower than bank transfers) 2. more convenient (you transact directly, cuts out the bank/credit card company middlemen). 3. fixed supply. 4. Greater alignment with our better human values. 5. The crypto system is digital technology. Traditional banking/payments is analogue technology, that cannot be upgraded; the entire architecture is antiquated 1970s technology cobbled together in a fit of absent-mindedness. Why is limited supply important for a currency? A currency that does not have limited supply is subject to inflation. Inflation is simply a way of measuring a reduction in your purchasing power. It is better called a Theft Index and is essentially a transfer of value from holders of nation state currencies to debtors. Usually, this happens just a little bit at a time, so you don’t notice the missing money and don’t freak out. Debtors benefit from inflation because it means that they have to repay less value, in real terms. Here is a chart of the purchasing power of the US dollar since the inception of the Federal Reserve to the end of 2017.  If you hold any nation state currency that doesn’t have a fixed supply, it is guaranteed that you will lose value. The US dollar has lost 95% of its value since the establishment of the Federal Reserve System in the US (which happened regardless of whether the country was on the gold standard or not). What can bitcoin do for society? Crypto currencies allow low income people to access a financial system. In the future, low income people everywhere will do their banking using the crypto system. The fractional reserve banking system has completely failed low income people. Of course, most poor people are not even accepted by these banks. The crypto system has significantly lower fixed costs than the traditional banking system and, consequently, allows everyone to benefit from financial inclusion. The poor will be able to make transfers at extremely low cost. Emerging crypto banks will allow them the benefits of the savings function, giving them the first opportunity ever to climb out of poverty. The effects for poor communities globally will be transformational. Here is a typical example of how banks treat those poor people who are fortunate enough even to have bank accounts. Bank of America will charge low-income customers $12 per month for their checking accounts unless they have a $1,500 account balance. @laura_nelson, Twitter, 2018 Finally, a bank with some fresh ideas on how to make poor people poorer. @kashanacauley, Twitter, 2018 Here is how blockchain is helping refugees. The UN's World Food Programme uses blockchain technology to provide identity and has distributed millions of dollars in food vouchers to tens of thousands of Syrian refugees in Jordan since May 2017. “The major benefit to the food program so far is a large drop in payments to financial services firms, the usual middlemen for transactions. Such fees have dropped ‘significantly,’ according to Houman Haddad”, the WFP executive leading the project. Quartz 3 Nov 2017. Note the major benefit: “the major benefit to the food program so far is a large drop in payments to financial services firms.” And what do banks think about bitcoin? A scam, used for buying drugs. Imagine them telling the truth: Well, people use it to make the lives of refugees better. Worse, it reduces the profits we make getting money to these refugee camps. So, it is really terrible. Asking a banker or central banker or their enablers what they think of bitcoin is like asking a taxi driver what he thinks about Uber. People like Jamie Dimon or Warren Buffett - one of the largest shareholders in Bank of America mentioned above. Maybe you don’t like the show of greed and all of the dodgy characters who tried to use crypto currencies to raise money, mostly for stupid projects, in 2018. No one does. But, you need to look beyond them to what bitcoin and blockchain can do for society. In the future, you will have to decide: do I stand with a community of people who want to make a better world, or do I stand with the 1% and their system of money and banking? Twitter: @ReassureFin |

| json metadata | {"tags":["bitcoin","blockchain","crypto","money","banking"],"users":["laura","kashanacauley","reassurefin"],"image":["https://cdn.steemitimages.com/DQmVxoNwZmEGeqC5pVidwiaagb59EwuWNxYwFNvJcjjGs1L/Invested%20house%20of%20cards%20main%20section.png","https://cdn.steemitimages.com/DQmTdGHWrfgwNP2dvRLbGGL28eFLHYQQBBtvYziPpz6xe5A/USD%20shitcoin%20in%20abstract.png"],"app":"steemit/0.1","format":"markdown"} |

| Transaction Info | Block #29311118/Trx fca004665a9758bdb3eeda921ee9e8db87b8f8ae |

View Raw JSON Data

{

"trx_id": "fca004665a9758bdb3eeda921ee9e8db87b8f8ae",

"block": 29311118,

"trx_in_block": 28,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-09T18:10:09",

"op": [

"comment",

{

"parent_author": "",

"parent_permlink": "bitcoin",

"author": "resreassure",

"permlink": "why-do-people-buy-bitcoin",

"title": "Why do people buy bitcoin?",

"body": "Why bitcoin?\n\nPeople buy bitcoin because of value and values.\n\nPeople buy bitcoin because it is a system of money that corresponds to how humanity has exchanged value for most of our history. Technologically, this system is based on mathematical formulae and a straight-forward verification and record system. The implications are spectacular: you can now trust exchanging value with another person or institution directly, even if you don’t know them.\n\nIn terms of values, the crypto system is profoundly natural, a very human invention, based on the concepts of freedom and fairness. It is the most authentic form of money humanity has had since value was based on memory. It is characterised as set out below.\n\nBased only on PV money (i.e. value that exists today, not tied to any required future value creation).\nAllows value to be exchanged directly between two parties without any bank middlemen, almost instantaneously and at extremely low cost.\nA better description than the term crypto currencies is honest money. This money system is about more than just exchanging value; it is also about our values. The crypto system is digital technology to banking and paper money’s analogue technology. The potential, the combination of value and values, that this new (old really) system unlocks for humanity is hard to overstate.\n\nThe fractional reserve banking system is intrinsically dishonest: bankers will tell you that your money is both safely in the bank and, at the same time, they are lending it out to others. They will tell you that it is your money while, legally, it belongs to the bank and they can do what they want with it.\n\n\n\nWhy is bitcoin superior to other currencies?\n\nBitcoin is a superior product to nation state currency and the fractional reserve banking system, for these reasons:\n\n1. lower cost (transaction costs much lower than bank transfers)\n2. more convenient (you transact directly, cuts out the bank/credit card company middlemen).\n3. fixed supply.\n4. Greater alignment with our better human values.\n5. The crypto system is digital technology. Traditional banking/payments is analogue technology, that cannot be upgraded; the entire architecture is antiquated 1970s technology cobbled together in a fit of absent-mindedness.\n\nWhy is limited supply important for a currency?\n\nA currency that does not have limited supply is subject to inflation. Inflation is simply a way of measuring a reduction in your purchasing power. It is better called a Theft Index and is essentially a transfer of value from holders of nation state currencies to debtors. Usually, this happens just a little bit at a time, so you don’t notice the missing money and don’t freak out. Debtors benefit from inflation because it means that they have to repay less value, in real terms.\n\nHere is a chart of the purchasing power of the US dollar since the inception of the Federal Reserve to the end of 2017.\n\n\n\nIf you hold any nation state currency that doesn’t have a fixed supply, it is guaranteed that you will lose value. The US dollar has lost 95% of its value since the establishment of the Federal Reserve System in the US (which happened regardless of whether the country was on the gold standard or not).\n\nWhat can bitcoin do for society?\n\nCrypto currencies allow low income people to access a financial system.\n\nIn the future, low income people everywhere will do their banking using the crypto system.\n\nThe fractional reserve banking system has completely failed low income people. Of course, most poor people are not even accepted by these banks. The crypto system has significantly lower fixed costs than the traditional banking system and, consequently, allows everyone to benefit from financial inclusion. The poor will be able to make transfers at extremely low cost. Emerging crypto banks will allow them the benefits of the savings function, giving them the first opportunity ever to climb out of poverty. The effects for poor communities globally will be transformational.\n\nHere is a typical example of how banks treat those poor people who are fortunate enough even to have bank accounts.\n\nBank of America will charge low-income customers $12 per month for their checking accounts unless they have a $1,500 account balance. @laura_nelson, Twitter, 2018\n\nFinally, a bank with some fresh ideas on how to make poor people poorer. @kashanacauley, Twitter, 2018\n\nHere is how blockchain is helping refugees.\n\nThe UN's World Food Programme uses blockchain technology to provide identity and has distributed millions of dollars in food vouchers to tens of thousands of Syrian refugees in Jordan since May 2017. “The major benefit to the food program so far is a large drop in payments to financial services firms, the usual middlemen for transactions. Such fees have dropped ‘significantly,’ according to Houman Haddad”, the WFP executive leading the project. Quartz 3 Nov 2017.\n\nNote the major benefit: “the major benefit to the food program so far is a large drop in payments to financial services firms.” And what do banks think about bitcoin? A scam, used for buying drugs.\n\nImagine them telling the truth: Well, people use it to make the lives of refugees better. Worse, it reduces the profits we make getting money to these refugee camps. So, it is really terrible.\n\nAsking a banker or central banker or their enablers what they think of bitcoin is like asking a taxi driver what he thinks about Uber.\n\nPeople like Jamie Dimon or Warren Buffett - one of the largest shareholders in Bank of America mentioned above.\n\nMaybe you don’t like the show of greed and all of the dodgy characters who tried to use crypto currencies to raise money, mostly for stupid projects, in 2018. No one does. But, you need to look beyond them to what bitcoin and blockchain can do for society.\n\nIn the future, you will have to decide: do I stand with a community of people who want to make a better world, or do I stand with the 1% and their system of money and banking?\n\n\nTwitter: @ReassureFin",

"json_metadata": "{\"tags\":[\"bitcoin\",\"blockchain\",\"crypto\",\"money\",\"banking\"],\"users\":[\"laura\",\"kashanacauley\",\"reassurefin\"],\"image\":[\"https://cdn.steemitimages.com/DQmVxoNwZmEGeqC5pVidwiaagb59EwuWNxYwFNvJcjjGs1L/Invested%20house%20of%20cards%20main%20section.png\",\"https://cdn.steemitimages.com/DQmTdGHWrfgwNP2dvRLbGGL28eFLHYQQBBtvYziPpz6xe5A/USD%20shitcoin%20in%20abstract.png\"],\"app\":\"steemit/0.1\",\"format\":\"markdown\"}"

}

]

}sensationupvoted (100.00%) @resreassure / crypto-and-the-payments-industry2019/01/07 21:54:18

sensationupvoted (100.00%) @resreassure / crypto-and-the-payments-industry

2019/01/07 21:54:18

| voter | sensation |

| author | resreassure |

| permlink | crypto-and-the-payments-industry |

| weight | 10000 (100.00%) |

| Transaction Info | Block #29258031/Trx eb56fa40ef2c7dc3b2b857b756e824578662653f |

View Raw JSON Data

{

"trx_id": "eb56fa40ef2c7dc3b2b857b756e824578662653f",

"block": 29258031,

"trx_in_block": 20,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-07T21:54:18",

"op": [

"vote",

{

"voter": "sensation",

"author": "resreassure",

"permlink": "crypto-and-the-payments-industry",

"weight": 10000

}

]

}magpieloverupvoted (100.00%) @resreassure / crypto-and-the-banking-industry2019/01/07 21:32:33

magpieloverupvoted (100.00%) @resreassure / crypto-and-the-banking-industry

2019/01/07 21:32:33

| voter | magpielover |

| author | resreassure |

| permlink | crypto-and-the-banking-industry |

| weight | 10000 (100.00%) |

| Transaction Info | Block #29257596/Trx 66fadfb4e0c4a118de15fd189e5aea26265feac1 |

View Raw JSON Data

{

"trx_id": "66fadfb4e0c4a118de15fd189e5aea26265feac1",

"block": 29257596,

"trx_in_block": 3,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-07T21:32:33",

"op": [

"vote",

{

"voter": "magpielover",

"author": "resreassure",

"permlink": "crypto-and-the-banking-industry",

"weight": 10000

}

]

}acknowledgementupvoted (10.00%) @resreassure / crypto-and-the-payments-industry2019/01/07 21:11:45

acknowledgementupvoted (10.00%) @resreassure / crypto-and-the-payments-industry

2019/01/07 21:11:45

| voter | acknowledgement |

| author | resreassure |

| permlink | crypto-and-the-payments-industry |

| weight | 1000 (10.00%) |

| Transaction Info | Block #29257181/Trx 64bdc56a408fefff81c639dacf4b8bda76f0b983 |

View Raw JSON Data

{

"trx_id": "64bdc56a408fefff81c639dacf4b8bda76f0b983",

"block": 29257181,

"trx_in_block": 1,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-07T21:11:45",

"op": [

"vote",

{

"voter": "acknowledgement",

"author": "resreassure",

"permlink": "crypto-and-the-payments-industry",

"weight": 1000

}

]

}acknowledgementupvoted (10.00%) @resreassure / crypto-and-the-banking-industry2019/01/07 21:11:18

acknowledgementupvoted (10.00%) @resreassure / crypto-and-the-banking-industry

2019/01/07 21:11:18

| voter | acknowledgement |

| author | resreassure |

| permlink | crypto-and-the-banking-industry |

| weight | 1000 (10.00%) |

| Transaction Info | Block #29257172/Trx 0a4bb93997d52008f669a55e4b69f23ded4243dd |

View Raw JSON Data

{

"trx_id": "0a4bb93997d52008f669a55e4b69f23ded4243dd",

"block": 29257172,

"trx_in_block": 35,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-07T21:11:18",

"op": [

"vote",

{

"voter": "acknowledgement",

"author": "resreassure",

"permlink": "crypto-and-the-banking-industry",

"weight": 1000

}

]

}2019/01/07 20:51:18

2019/01/07 20:51:18

| parent author | resreassure |

| parent permlink | crypto-and-the-banking-industry |

| author | cheetah |

| permlink | cheetah-re-resreassurecrypto-and-the-banking-industry |

| title | |

| body | Hi! I am a robot. I just upvoted you! I found similar content that readers might be interested in: https://www.cryptopedic.com/news/the-crypto-system-will-replace-the-banking-system-in-the-next-decade/ |

| json metadata | |

| Transaction Info | Block #29256772/Trx c69fc1249008942a6333dea159ddd1bbef7dd603 |

View Raw JSON Data

{

"trx_id": "c69fc1249008942a6333dea159ddd1bbef7dd603",

"block": 29256772,

"trx_in_block": 18,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-07T20:51:18",

"op": [

"comment",

{

"parent_author": "resreassure",

"parent_permlink": "crypto-and-the-banking-industry",

"author": "cheetah",

"permlink": "cheetah-re-resreassurecrypto-and-the-banking-industry",

"title": "",

"body": "Hi! I am a robot. I just upvoted you! I found similar content that readers might be interested in:\nhttps://www.cryptopedic.com/news/the-crypto-system-will-replace-the-banking-system-in-the-next-decade/",

"json_metadata": ""

}

]

}cheetahupvoted (0.08%) @resreassure / crypto-and-the-banking-industry2019/01/07 20:51:15

cheetahupvoted (0.08%) @resreassure / crypto-and-the-banking-industry

2019/01/07 20:51:15

| voter | cheetah |

| author | resreassure |

| permlink | crypto-and-the-banking-industry |

| weight | 8 (0.08%) |

| Transaction Info | Block #29256771/Trx ed18eabdf7fbabf108131cb8ea0000dd41b754a7 |

View Raw JSON Data

{

"trx_id": "ed18eabdf7fbabf108131cb8ea0000dd41b754a7",

"block": 29256771,

"trx_in_block": 11,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-07T20:51:15",

"op": [

"vote",

{

"voter": "cheetah",

"author": "resreassure",

"permlink": "crypto-and-the-banking-industry",

"weight": 8

}

]

}resreassureupdated options for crypto-and-the-banking-industry2019/01/07 20:51:03

resreassureupdated options for crypto-and-the-banking-industry

2019/01/07 20:51:03

| author | resreassure |

| permlink | crypto-and-the-banking-industry |

| max accepted payout | 0.000 SBD |

| percent steem dollars | 10000 |

| allow votes | true |

| allow curation rewards | true |

| extensions | [] |

| Transaction Info | Block #29256767/Trx b265053d1f1af4875682427c5ac8b6a0d43751e3 |

View Raw JSON Data

{

"trx_id": "b265053d1f1af4875682427c5ac8b6a0d43751e3",

"block": 29256767,

"trx_in_block": 25,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-07T20:51:03",

"op": [

"comment_options",

{

"author": "resreassure",

"permlink": "crypto-and-the-banking-industry",

"max_accepted_payout": "0.000 SBD",

"percent_steem_dollars": 10000,

"allow_votes": true,

"allow_curation_rewards": true,

"extensions": []

}

]

}resreassurepublished a new post: crypto-and-the-banking-industry2019/01/07 20:51:03

resreassurepublished a new post: crypto-and-the-banking-industry

2019/01/07 20:51:03

| parent author | |

| parent permlink | blockchain |

| author | resreassure |

| permlink | crypto-and-the-banking-industry |

| title | Crypto and the banking industry |

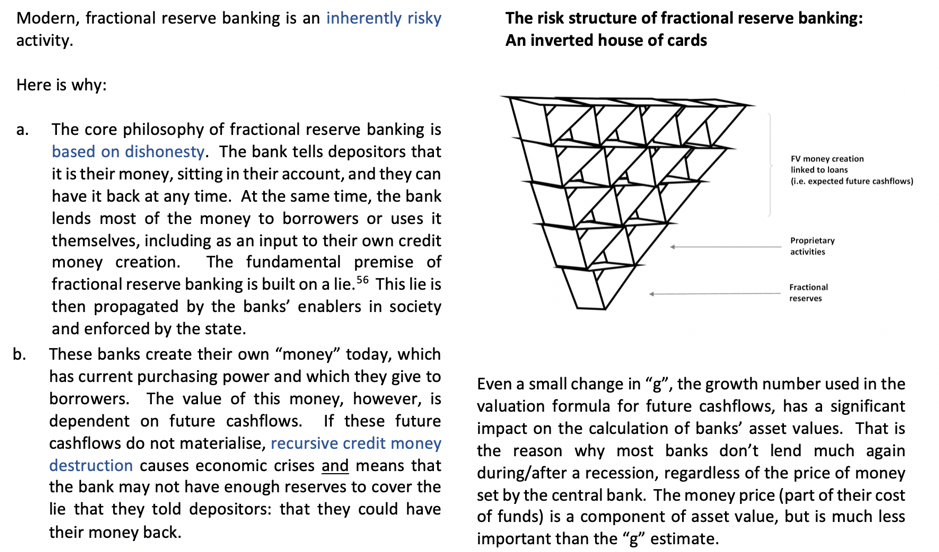

| body | Here is a little comparison of the crypto system and our current banking system. **Superior value and better values** Crypto currencies are a superior product to nation state currency and the fractional reserve banking system, for these reasons: 1. lower cost (transaction costs much lower than bank transfers) 2. more convenient (you transact directly, cuts out the bank/credit card company middlemen). 3. fixed supply. 4. Greater alignment with our better human values. The crypto system is digital technology. Traditional banking/payments is analogue technology, that cannot be upgraded; the entire architecture is antiquated 1970s technology cobbled together in a fit of absent-mindedness. Crypto is your smart phone. The banking system is like using a Blackberry. The payments system is like using a rotary dial fixed line phone. **Adoption** The biggest obstacle to crypto currencies is access to the real economy. The entities preventing this access are banks and their enablers. When a crypto bank emerges (in 2019) that links crypto to the real economy, adoption will increase exponentially.  **Our current banking system** The fractional reserve banking system is intrinsically dishonest: bankers will tell you that your money is both safely in the bank and, at the same time, they are lending it out to others. They will tell you that it is your money while, legally, it belongs to the bank and they can do what they want with it.  **The crypto system** In 2009 Satoshi Nakamoto created a system of money that corresponds to how humanity has exchanged value for most of our history. Technologically, this system is based on mathematical formulae and a straight-forward verification and record system. The implications are spectacular: you can now trust exchanging value with another person or institution directly, even if you don’t know them. In terms of values, the crypto system is profoundly natural, a very human invention, based on the concepts of freedom and fairness. It is the most authentic form of money humanity has had since value was based on memory. It is characterised as set out below. 1. Based only on PV money (i.e. value that exists today, not tied to any required future value creation). 2. Allows value to be exchanged directly between two parties without any bank middlemen, almost instantaneously and at extremely low cost. A better description than the term crypto currencies is honest money. This money system is about more than just exchanging value; it is also about our values. The potential, the combination of value and values, that this new (old really) system unlocks for humanity is hard to overstate. **The future** The crypto system will offer higher returns for less risk and depositors will increasingly vote with their feet. Over the next decade, the crypto system will expand and the fractional reserve banking system will decline. An inflection point will be reached where the rate of change for both accelerates rapidly. The fractional reserve system is intrinsically structured like an inverted house of cards. Once enough deposits are pulled out of the bottom, the house will collapse. Asking a banker what he thinks about crypto is like asking a taxi driver what he thinks about Uber. The crypto system is an existential threat to nation state currency as well as to the fractional reserve banking system and to their enablers. It is incompatible with fractional reserve banking. The crypto system is based on a transparent record of truth, captured forever in a giant record paper, and on value that exists today. Only one of these two systems can survive. They cannot co-exist together in the long-term. They are not going to be best friends, give each other warm hugs, and talk about a win-win paradigm. Their values are completely contradictory. Expect the banks and their enablers to continue to be relentless and underhanded when attacking the crypto system.  *I’m delighted to join your Enterprise Alliance, my naive young Russian Canadian friend.* Twitter: @ReassureFin |

| json metadata | {"tags":["blockchain","crypto","banking","finance","money"],"users":["reassurefin"],"image":["https://cdn.steemitimages.com/DQmWU411mBwx7P8zQk8qWfHR56N3inPMFNSLabaQm3v1Ebu/Crypto%20puzzle.png","https://cdn.steemitimages.com/DQmVxoNwZmEGeqC5pVidwiaagb59EwuWNxYwFNvJcjjGs1L/Invested%20house%20of%20cards%20main%20section.png","https://cdn.steemitimages.com/DQmWm5UszLWiWMBTCv1UhwrLeppKVUoGQSQE8XWesXp7CfF/Wolf%20in%20sheeps%20clothing.png"],"app":"steemit/0.1","format":"markdown"} |

| Transaction Info | Block #29256767/Trx b265053d1f1af4875682427c5ac8b6a0d43751e3 |

View Raw JSON Data

{

"trx_id": "b265053d1f1af4875682427c5ac8b6a0d43751e3",

"block": 29256767,

"trx_in_block": 25,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-07T20:51:03",

"op": [

"comment",

{

"parent_author": "",

"parent_permlink": "blockchain",

"author": "resreassure",

"permlink": "crypto-and-the-banking-industry",

"title": "Crypto and the banking industry",

"body": "Here is a little comparison of the crypto system and our current banking system.\n\n**Superior value and better values**\n\nCrypto currencies are a superior product to nation state currency and the fractional reserve banking system, for these reasons:\n\n1. lower cost (transaction costs much lower than bank transfers)\n2. more convenient (you transact directly, cuts out the bank/credit card company middlemen).\n3. fixed supply.\n4. Greater alignment with our better human values.\n\nThe crypto system is digital technology. Traditional banking/payments is analogue technology, that cannot be upgraded; the entire architecture is antiquated 1970s technology cobbled together in a fit of absent-mindedness. Crypto is your smart phone. The banking system is like using a Blackberry. The payments system is like using a rotary dial fixed line phone.\n\n**Adoption**\n\nThe biggest obstacle to crypto currencies is access to the real economy. The entities preventing this access are banks and their enablers. When a crypto bank emerges (in 2019) that links crypto to the real economy, adoption will increase exponentially. \n\n\n\n**Our current banking system** \n\nThe fractional reserve banking system is intrinsically dishonest: bankers will tell you that your money is both safely in the bank and, at the same time, they are lending it out to others. They will tell you that it is your money while, legally, it belongs to the bank and they can do what they want with it. \n\n\n\n**The crypto system** \n\nIn 2009 Satoshi Nakamoto created a system of money that corresponds to how humanity has exchanged value for most of our history. Technologically, this system is based on mathematical formulae and a straight-forward verification and record system. The implications are spectacular: you can now trust exchanging value with another person or institution directly, even if you don’t know them. \n\nIn terms of values, the crypto system is profoundly natural, a very human invention, based on the concepts of freedom and fairness. It is the most authentic form of money humanity has had since value was based on memory. It is characterised as set out below.\n\n1. Based only on PV money (i.e. value that exists today, not tied to any required future value creation).\n2. Allows value to be exchanged directly between two parties without any bank middlemen, almost instantaneously and at extremely low cost. \n\nA better description than the term crypto currencies is honest money. This money system is about more than just exchanging value; it is also about our values. The potential, the combination of value and values, that this new (old really) system unlocks for humanity is hard to overstate. \n\n**The future**\n\nThe crypto system will offer higher returns for less risk and depositors will increasingly vote with their feet. Over the next decade, the crypto system will expand and the fractional reserve banking system will decline. An inflection point will be reached where the rate of change for both accelerates rapidly. The fractional reserve system is intrinsically structured like an inverted house of cards. Once enough deposits are pulled out of the bottom, the house will collapse. Asking a banker what he thinks about crypto is like asking a taxi driver what he thinks about Uber. \n\nThe crypto system is an existential threat to nation state currency as well as to the fractional reserve banking system and to their enablers. It is incompatible with fractional reserve banking. The crypto system is based on a transparent record of truth, captured forever in a giant record paper, and on value that exists today. \n\nOnly one of these two systems can survive. They cannot co-exist together in the long-term. They are not going to be best friends, give each other warm hugs, and talk about a win-win paradigm. Their values are completely contradictory. Expect the banks and their enablers to continue to be relentless and underhanded when attacking the crypto system. \n\n\n*I’m delighted to join your Enterprise Alliance, my naive young Russian Canadian friend.* \n\n\nTwitter: @ReassureFin",

"json_metadata": "{\"tags\":[\"blockchain\",\"crypto\",\"banking\",\"finance\",\"money\"],\"users\":[\"reassurefin\"],\"image\":[\"https://cdn.steemitimages.com/DQmWU411mBwx7P8zQk8qWfHR56N3inPMFNSLabaQm3v1Ebu/Crypto%20puzzle.png\",\"https://cdn.steemitimages.com/DQmVxoNwZmEGeqC5pVidwiaagb59EwuWNxYwFNvJcjjGs1L/Invested%20house%20of%20cards%20main%20section.png\",\"https://cdn.steemitimages.com/DQmWm5UszLWiWMBTCv1UhwrLeppKVUoGQSQE8XWesXp7CfF/Wolf%20in%20sheeps%20clothing.png\"],\"app\":\"steemit/0.1\",\"format\":\"markdown\"}"

}

]

}resreassureupdated options for crypto-and-the-payments-industry2019/01/07 20:45:12

resreassureupdated options for crypto-and-the-payments-industry

2019/01/07 20:45:12

| author | resreassure |

| permlink | crypto-and-the-payments-industry |

| max accepted payout | 0.000 SBD |

| percent steem dollars | 10000 |

| allow votes | true |

| allow curation rewards | true |

| extensions | [] |

| Transaction Info | Block #29256650/Trx 5c3a1fdefc1897906c7e1a50c8d3fb59919ac0e5 |

View Raw JSON Data

{

"trx_id": "5c3a1fdefc1897906c7e1a50c8d3fb59919ac0e5",

"block": 29256650,

"trx_in_block": 25,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-07T20:45:12",

"op": [

"comment_options",

{

"author": "resreassure",

"permlink": "crypto-and-the-payments-industry",

"max_accepted_payout": "0.000 SBD",

"percent_steem_dollars": 10000,

"allow_votes": true,

"allow_curation_rewards": true,

"extensions": []

}

]

}resreassurepublished a new post: crypto-and-the-payments-industry2019/01/07 20:45:12

resreassurepublished a new post: crypto-and-the-payments-industry

2019/01/07 20:45:12

| parent author | |

| parent permlink | crypto |

| author | resreassure |

| permlink | crypto-and-the-payments-industry |

| title | Crypto and the payments industry |

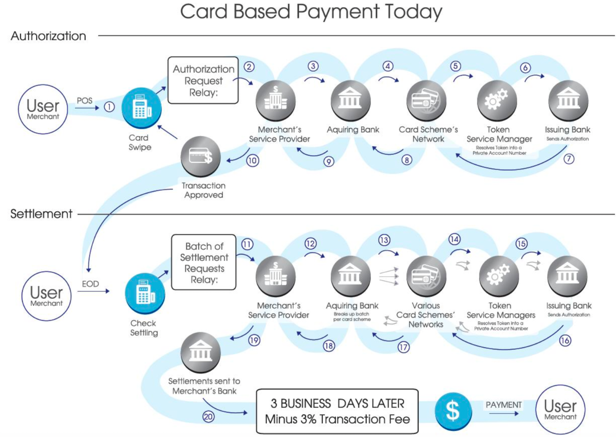

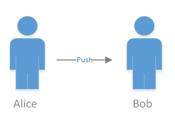

| body | The crypto system will replace the current payments industry in the next decade. Here is why. **Current system** The existing cards - banking system is based on pull technology, which is complex, costly and prone to fraud. The crypto payment system, based on push technology, is simpler than and will replace the old system. A decade from now no one will use the pull-based system; it will completely disappear. The plumbing necessary for credit card payments, combined with the traditional banking industry, is illustrated below.  Add another 5–8 steps for cross-border payments. If it looks like it was cobbled together in a fit of absent-mindedness based on 1970s technology, that is because it was. The biggest weakness in the payment system is security, which is vastly inferior to the crypto system. **Crypto system** Here is how the crypto payment system works:[1]  Visa, Mastercard, JCB, UnionPay: they will all face their Kodak moment in the next decade. Same for PayPal, Square, makers of point of sale equipment, etc. It is like fixed telephone line switchboard systems: no longer needed. Of course, people won't stop using credit cards overnight, but most people will not have a credit card a decade from now. But, bankruptcy? There are two important things to realise about the structure of the credit card processor industry (in addition to the vastly inferior technology): it has a high break-even point and a large number of self-interested, uncoordinated participants fighting for industry profits. Think they might adapt to the crypto system? Maybe about as easily as a school of fish might adapt to using bicycles as a new means of getting around. **Merchants will drive the change** The main impetus for switching from credit cards to crypto system payments will come from merchants. The average credit card processing cost for a retail business where cards are swiped is roughly 1.90%-2.15% for Visa and Mastercard transactions. The average cost for card-not-present transactions, such as online, is roughly 2.30%-2.50%. Worse, long transaction reconciliation times have a negative impact on merchant's working capital. With credit cards, maybe you think you have paid for that latte right away, but the money reaches the merchant days later. The merchant also bears the risk of chargebacks for a considerable period of time after: typically for up to 90–120 calendar days (based on a "Central Site Business Date"). Chargeback costs to merchants is expected to reach $31 billion by 2020.[2] In 2016, only 23% of chargebacks were in relation to identity theft. So-called "friendly fraud" accounted for 28% and "chargeback fraud" accounted for another 28%.[3] In comparison, with the crypto system the merchant gets the money right away. With the push system, the crypto system, there are no chargebacks. For the merchant, the best comparison is money in about 3 business days with no finality for a total of 90–120 days at a cost of maybe 2%, versus an x second/minute block time in crypto with finality and at zero cost. **Lack of security with the current system** The other major difference between the soon-to-die credit card push system and the crypto system that will replace it is security. With your credit card, you are not actually making a payment. What you are doing is giving an approval (based on your Personal Account Number) to the merchant to pull money from your account. Since the merchant is just the end link in the payments chain, the merchant's system needs to transmit your account details to every other entity in the process. So, you, the customer, effectively have to trust all of the 20 parties in this chain. Payment processors biggest cost is security; they spend billions each year on trying to prevent fraud. Think maybe you were not affected? In 2017, the Identity Theft Resource Center counted 1,579 data breaches in the United States, up 45 percent from 2016, affecting 178,955,069 records.[4] Credit card fraud in the US exceeded $7 billion in 2017.[5]In the United Kingdom, 4.7 million people reported their credit card lost or stolen or misused, with an average loss per person of £833 pounds.[6] Financial institutions globally are expected to spend $9.2 billion by 2020 to prevent credit card fraud.[7] In the crypto system, what keeps push payments from A to B (which could be individuals, or an individual to a merchant, or a business to a business) safe is simple and based on: (1) keeping your private keys (basically a long complex password) secure and (2) the community working together, based on economic incentives to keep the system database protected. All system users basically contribute a small amount to a diverse group of system supporters to ensure that it remains safe. The crypto system is mathematically almost impossible to break. There are some weak points (like exchanges, which are just SQL databases) but these are not part of the crypto system. In the crypto system, security costs are a tiny fraction of the amount spent by traditional players. To criticise the crypto system for excessive electricity costs is simply the big lie strategy: it isn't comparing the role the miners play in the system to the equivalent functions required in the fractional reserve banking and payments systems and by society. Losses in the genuine crypto system are almost non-existent, compared to an astronomical amount of money lost to payments fraud. The only effective way to eliminate payment fraud almost entirely and the costs of trying to prevent this fraud is to adopt the crypto system. **Trilemma issue and lattes** Vitalik Buterin has the annoying trait of being really honest and open about technical issues in the crypto system. In respect of payments, this is the scalability trilemma, which posits that (at the moment) a blockchain cannot have all three of these characteristics at the same time: decentralised, scalable, and secure; it can only have two of the three. It allows bank-funded economists to ignore the superiority of the crypto system over the fractional reserve banking system and the payments system and focus on issues important to them: the horrifying possibility of cold lattes. Being rude to Vitalik for slow processing[8]and concluding that the crypto system will never reach its potential is like yelling at Gordon Moore in the 1960s that there are not enough transistors on a microchip to do anything useful. First, tech scales exponentially; it is a bad idea to bet against that. Second, there are also many interim solutions. With a proper crypto bank, for example, the crypto bank could guarantee to the merchant the availability of funds immediately, even if it will take a few minutes after to settle on the blockchain. Third, the criticism applies to small payments where speed is important, but there is a vast market for larger payments where settlement could be in minutes, not seconds, and still be vastly superior to the present system. That is why crypto transfers will start at the larger end: payment for large shipments of coffee beans can take days to process through the banking system. In this part of the chain, commodity players would be ecstatic to wait 10 minutes for confirmation and finality. Twitter: @ReassureFin --- [1] You could add some minor complexity, like wallet details or maybe Alice and Bob will use a form of a crypto bank in the future, but the heart of the push system in crypto is just this simple. [2] The Nilson Report, 2017. [3] LexisNexis 2016 True Cost of Fraud study. [4] Note: only covers those data breaches notified by companies to authorities. Of these notified breaches, 37% of notifications did not quantify the number of records - such as Social Security numbers and payment card data - that was exposed. [5] FT Partners Research and Statistica. [6] Report commissioned by Comparethemarket.com, for the last 12 months to July 2018. [7] Juniper Research, Online Payment Fraud: Key Vertical Strategies and Management 2015–16. [8] From the latte buyer's, not the merchant's perspective. |

| json metadata | {"tags":["crypto","payments","banking","finance","blockchain"],"users":["reassurefin"],"image":["https://cdn.steemitimages.com/DQmPkewgHzs44BCrBfZ2v4cY9kpFuxT1e3f3SVWSMs1vbUd/Card%20payment%20what%20a%20joke%20in%2021st%20century.png","https://cdn.steemitimages.com/DQmV9Q5SML8ZAnkqjKrw4CKqyRaJokb7UgHea3Gf2i2hYUj/Alice%20Bob.png"],"app":"steemit/0.1","format":"markdown"} |

| Transaction Info | Block #29256650/Trx 5c3a1fdefc1897906c7e1a50c8d3fb59919ac0e5 |

View Raw JSON Data

{

"trx_id": "5c3a1fdefc1897906c7e1a50c8d3fb59919ac0e5",

"block": 29256650,

"trx_in_block": 25,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-07T20:45:12",

"op": [

"comment",

{

"parent_author": "",

"parent_permlink": "crypto",

"author": "resreassure",

"permlink": "crypto-and-the-payments-industry",

"title": "Crypto and the payments industry",

"body": "The crypto system will replace the current payments industry in the next decade. Here is why. \n\n**Current system**\n\nThe existing cards - banking system is based on pull technology, which is complex, costly and prone to fraud. The crypto payment system, based on push technology, is simpler than and will replace the old system. A decade from now no one will use the pull-based system; it will completely disappear.\n\nThe plumbing necessary for credit card payments, combined with the traditional banking industry, is illustrated below. \n\n\n\nAdd another 5–8 steps for cross-border payments.\n\nIf it looks like it was cobbled together in a fit of absent-mindedness based on 1970s technology, that is because it was.\n\nThe biggest weakness in the payment system is security, which is vastly inferior to the crypto system.\n\n**Crypto system**\n\nHere is how the crypto payment system works:[1]\n\n\n\nVisa, Mastercard, JCB, UnionPay: they will all face their Kodak moment in the next decade. Same for PayPal, Square, makers of point of sale equipment, etc. It is like fixed telephone line switchboard systems: no longer needed.\n\nOf course, people won't stop using credit cards overnight, but most people will not have a credit card a decade from now. \n\nBut, bankruptcy? There are two important things to realise about the structure of the credit card processor industry (in addition to the vastly inferior technology): it has a high break-even point and a large number of self-interested, uncoordinated participants fighting for industry profits. Think they might adapt to the crypto system? Maybe about as easily as a school of fish might adapt to using bicycles as a new means of getting around.\n\n**Merchants will drive the change**\n\nThe main impetus for switching from credit cards to crypto system payments will come from merchants. The average credit card processing cost for a retail business where cards are swiped is roughly 1.90%-2.15% for Visa and Mastercard transactions. The average cost for card-not-present transactions, such as online, is roughly 2.30%-2.50%. \n\nWorse, long transaction reconciliation times have a negative impact on merchant's working capital. With credit cards, maybe you think you have paid for that latte right away, but the money reaches the merchant days later. The merchant also bears the risk of chargebacks for a considerable period of time after: typically for up to 90–120 calendar days (based on a \"Central Site Business Date\"). Chargeback costs to merchants is expected to reach $31 billion by 2020.[2] In 2016, only 23% of chargebacks were in relation to identity theft. So-called \"friendly fraud\" accounted for 28% and \"chargeback fraud\" accounted for another 28%.[3]\n\nIn comparison, with the crypto system the merchant gets the money right away. With the push system, the crypto system, there are no chargebacks. For the merchant, the best comparison is money in about 3 business days with no finality for a total of 90–120 days at a cost of maybe 2%, versus an x second/minute block time in crypto with finality and at zero cost.\n\n**Lack of security with the current system**\n\nThe other major difference between the soon-to-die credit card push system and the crypto system that will replace it is security. With your credit card, you are not actually making a payment. What you are doing is giving an approval (based on your Personal Account Number) to the merchant to pull money from your account. Since the merchant is just the end link in the payments chain, the merchant's system needs to transmit your account details to every other entity in the process. So, you, the customer, effectively have to trust all of the 20 parties in this chain. Payment processors biggest cost is security; they spend billions each year on trying to prevent fraud. Think maybe you were not affected? In 2017, the Identity Theft Resource Center counted 1,579 data breaches in the United States, up 45 percent from 2016, affecting 178,955,069 records.[4] Credit card fraud in the US exceeded $7 billion in 2017.[5]In the United Kingdom, 4.7 million people reported their credit card lost or stolen or misused, with an average loss per person of £833 pounds.[6] Financial institutions globally are expected to spend $9.2 billion by 2020 to prevent credit card fraud.[7]\n\nIn the crypto system, what keeps push payments from A to B (which could be individuals, or an individual to a merchant, or a business to a business) safe is simple and based on: (1) keeping your private keys (basically a long complex password) secure and (2) the community working together, based on economic incentives to keep the system database protected. All system users basically contribute a small amount to a diverse group of system supporters to ensure that it remains safe. \n\nThe crypto system is mathematically almost impossible to break. There are some weak points (like exchanges, which are just SQL databases) but these are not part of the crypto system. \n\nIn the crypto system, security costs are a tiny fraction of the amount spent by traditional players. To criticise the crypto system for excessive electricity costs is simply the big lie strategy: it isn't comparing the role the miners play in the system to the equivalent functions required in the fractional reserve banking and payments systems and by society. Losses in the genuine crypto system are almost non-existent, compared to an astronomical amount of money lost to payments fraud. The only effective way to eliminate payment fraud almost entirely and the costs of trying to prevent this fraud is to adopt the crypto system.\n\n**Trilemma issue and lattes**\n\nVitalik Buterin has the annoying trait of being really honest and open about technical issues in the crypto system. In respect of payments, this is the scalability trilemma, which posits that (at the moment) a blockchain cannot have all three of these characteristics at the same time: decentralised, scalable, and secure; it can only have two of the three. It allows bank-funded economists to ignore the superiority of the crypto system over the fractional reserve banking system and the payments system and focus on issues important to them: the horrifying possibility of cold lattes.\n\nBeing rude to Vitalik for slow processing[8]and concluding that the crypto system will never reach its potential is like yelling at Gordon Moore in the 1960s that there are not enough transistors on a microchip to do anything useful. First, tech scales exponentially; it is a bad idea to bet against that. Second, there are also many interim solutions. With a proper crypto bank, for example, the crypto bank could guarantee to the merchant the availability of funds immediately, even if it will take a few minutes after to settle on the blockchain. Third, the criticism applies to small payments where speed is important, but there is a vast market for larger payments where settlement could be in minutes, not seconds, and still be vastly superior to the present system. That is why crypto transfers will start at the larger end: payment for large shipments of coffee beans can take days to process through the banking system. In this part of the chain, commodity players would be ecstatic to wait 10 minutes for confirmation and finality.\n\nTwitter: @ReassureFin\n\n\n---\n\n[1] You could add some minor complexity, like wallet details or maybe Alice and Bob will use a form of a crypto bank in the future, but the heart of the push system in crypto is just this simple.\n[2] The Nilson Report, 2017.\n[3] LexisNexis 2016 True Cost of Fraud study.\n[4] Note: only covers those data breaches notified by companies to authorities. Of these notified breaches, 37% of notifications did not quantify the number of records - such as Social Security numbers and payment card data - that was exposed.\n[5] FT Partners Research and Statistica.\n[6] Report commissioned by Comparethemarket.com, for the last 12 months to July 2018.\n[7] Juniper Research, Online Payment Fraud: Key Vertical Strategies and Management 2015–16.\n[8] From the latte buyer's, not the merchant's perspective.",

"json_metadata": "{\"tags\":[\"crypto\",\"payments\",\"banking\",\"finance\",\"blockchain\"],\"users\":[\"reassurefin\"],\"image\":[\"https://cdn.steemitimages.com/DQmPkewgHzs44BCrBfZ2v4cY9kpFuxT1e3f3SVWSMs1vbUd/Card%20payment%20what%20a%20joke%20in%2021st%20century.png\",\"https://cdn.steemitimages.com/DQmV9Q5SML8ZAnkqjKrw4CKqyRaJokb7UgHea3Gf2i2hYUj/Alice%20Bob.png\"],\"app\":\"steemit/0.1\",\"format\":\"markdown\"}"

}

]

}sensationupvoted (100.00%) @resreassure / a-history-of-money2019/01/05 16:53:39

sensationupvoted (100.00%) @resreassure / a-history-of-money

2019/01/05 16:53:39

| voter | sensation |

| author | resreassure |

| permlink | a-history-of-money |

| weight | 10000 (100.00%) |

| Transaction Info | Block #29194475/Trx a45f155c8fe01dc177c310b6f41b98418b9413a3 |

View Raw JSON Data

{

"trx_id": "a45f155c8fe01dc177c310b6f41b98418b9413a3",

"block": 29194475,

"trx_in_block": 3,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-05T16:53:39",

"op": [

"vote",

{

"voter": "sensation",

"author": "resreassure",

"permlink": "a-history-of-money",

"weight": 10000

}

]

}cmadupvoted (100.00%) @resreassure / crypto-and-sex2019/01/05 15:56:00

cmadupvoted (100.00%) @resreassure / crypto-and-sex

2019/01/05 15:56:00

| voter | cmad |

| author | resreassure |

| permlink | crypto-and-sex |

| weight | 10000 (100.00%) |

| Transaction Info | Block #29193324/Trx 5633ed4aa9294712c54acb16a9e043cb83ae99aa |

View Raw JSON Data

{

"trx_id": "5633ed4aa9294712c54acb16a9e043cb83ae99aa",

"block": 29193324,

"trx_in_block": 4,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-05T15:56:00",

"op": [

"vote",

{

"voter": "cmad",

"author": "resreassure",

"permlink": "crypto-and-sex",

"weight": 10000

}

]

}2019/01/05 15:55:36

2019/01/05 15:55:36

| voter | sensation |

| author | resreassure |

| permlink | the-crypto-system-will-replace-the-banking-system-in-the-next-decade-and-other-predictions |

| weight | 10000 (100.00%) |

| Transaction Info | Block #29193316/Trx 30027b32db67b3f023afe2e3f0251af91aaa8d59 |

View Raw JSON Data

{

"trx_id": "30027b32db67b3f023afe2e3f0251af91aaa8d59",

"block": 29193316,

"trx_in_block": 15,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-05T15:55:36",

"op": [

"vote",

{

"voter": "sensation",

"author": "resreassure",

"permlink": "the-crypto-system-will-replace-the-banking-system-in-the-next-decade-and-other-predictions",

"weight": 10000

}

]

}resreassureupdated options for a-history-of-money2019/01/05 15:25:03

resreassureupdated options for a-history-of-money

2019/01/05 15:25:03

| author | resreassure |

| permlink | a-history-of-money |

| max accepted payout | 0.000 SBD |

| percent steem dollars | 10000 |

| allow votes | true |

| allow curation rewards | true |

| extensions | [] |

| Transaction Info | Block #29192705/Trx 1413b46de496016705d780efb297f57715feb1ed |

View Raw JSON Data

{

"trx_id": "1413b46de496016705d780efb297f57715feb1ed",

"block": 29192705,

"trx_in_block": 29,

"op_in_trx": 0,

"virtual_op": 0,

"timestamp": "2019-01-05T15:25:03",

"op": [

"comment_options",

{

"author": "resreassure",

"permlink": "a-history-of-money",

"max_accepted_payout": "0.000 SBD",

"percent_steem_dollars": 10000,

"allow_votes": true,

"allow_curation_rewards": true,

"extensions": []

}

]

}resreassurepublished a new post: a-history-of-money2019/01/05 15:25:03

resreassurepublished a new post: a-history-of-money

2019/01/05 15:25:03

| parent author | |

| parent permlink | crypto |

| author | resreassure |

| permlink | a-history-of-money |

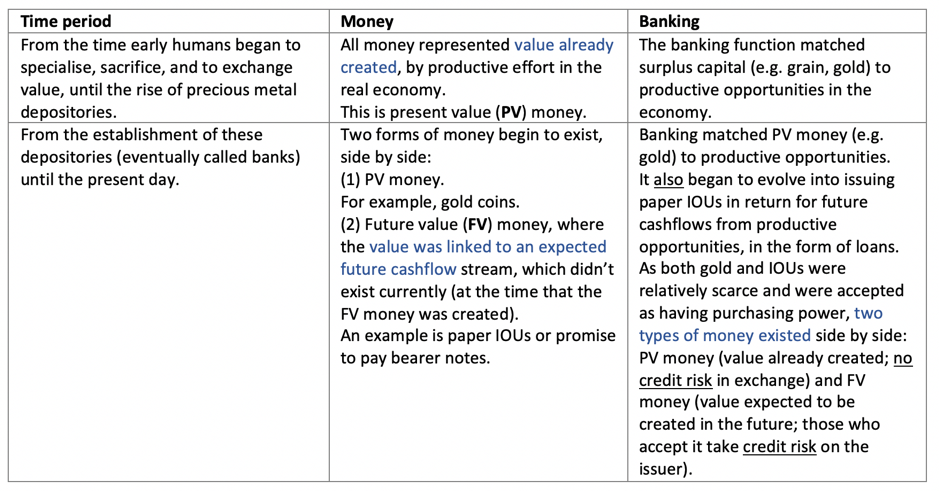

| title | A history of money |